Health insurance. It’s two words that can spark confusion, frustration, and anxiety all at once. Whether you’re typing “what is a health insurance card,” searching for the “#1 health insurance company,” or desperately trying to find “$0 a month ACA health insurance,” you’ve come to the right place.

This master article is designed as your comprehensive encyclopedia. We have taken every keyword—from the basics of your insurance card to the nuances of coverage for seniors, parents, and even 7-Eleven employees—and built a complete reference guide for 2026.

What You Will Learn (Jump to Any Section):

- Part 1: The Fundamentals (Your Health Insurance Card & Basic Terms)

- Part 2: The Best of the Best (#1 Companies & Top 10 Lists)

- Part 3: The Cost Question ($0 Plans & Deductibles Explained)

- Part 4: Timing & Duration (1 Month, 30 Day, & COBRA Plans)

- Part 5: Demographics (Seniors, Parents, & Young Adults)

- Part 6: Special Situations (Employer Coverage & Short-Term Gaps)

Part 1: The Fundamentals (Your Health Insurance Card & Basic Definitions)

Before we compare billion-dollar companies, let’s start with the plastic rectangle in your wallet.

What is a Health Insurance Card?

Your health insurance card (often called an ID card) is your proof of coverage. When you check into a doctor’s office or hospital, this is the first thing they ask for.

Every card contains these 5 critical fields:

- Member ID Number: Your unique identifier for the insurer (similar to a student ID).

- Group Number: Identifies your specific employer or plan pool.

- Copay Amounts: Often listed as “PCP 25″(PrimaryCarePhysician)or”Specialist25″(PrimaryCarePhysician)or“Specialist50.”

- Deductible Status: Some cards show how much of your deductible you have met.

- Network Logo: Look for PPO, HMO, EPO, or POS to know which doctors you can see.

Pro Tip: Take a photo of the front and back of your card immediately. If you lose your wallet, you still have the info needed to fill a prescription or check into an ER.

What is “#1 Health Insurance”?

There is no single “best” plan for everyone, but there are carriers that consistently rank highest for customer service, network size, and financial stability.

What does “#1” refer to?

- Largest by Market Share: UnitedHealthcare (often cited as #1).

- Best Customer Satisfaction: Often Blue Cross Blue Shield (BCBS) or Kaiser Permanente.

- Cheapest for Low Income: The ACA Marketplace, which offers subsidies so large that 92% of Texas enrollees pay very little.

Part 2: The Best of the Best (Rankings & Top 10 Lists)

If you are searching for the “#1 health insurance company” or the “#1 health insurance company in the US,” you need to look at three different metrics: size, value, and quality.

The “Big 5” National Carriers (2026)

These are the giants you will encounter on almost every search engine.

- UnitedHealthcare (UHC): The largest by revenue and membership. Excellent for national PPO networks.

- Anthem (BCBS): Largest provider network in most states.

- Kaiser Permanente: Highest rated for quality, but only available in specific regions (mostly West Coast & Mid-Atlantic).

- Cigna: Great for global mobility and wellness programs.

- Humana: Dominant in the Medicare Advantage (65+) space.

10 Top Health Insurance Companies (The Industry Leaders)

For 2026, these are the names you will see dominating ACA Marketplaces and employer lists. The “top” ranking depends on your state, but nationally these 10 have the largest footprints and best financial ratings (AM Best A or higher):

- 1. UnitedHealthcare (Largest network)

- 2. Blue Cross Blue Shield (Most accepted nationwide)

- 3. Kaiser Permanente (Highest member satisfaction)

- 4. Elevance Health (Anthem)

- 5. Cigna

- 6. Humana

- 7. Centene (Ambetter) (Dominates ACA Marketplace plans)

- 8. Molina Healthcare (Strong with Medicaid)

- 9. Aetna (CVS Health)

- 10. Oscar Health (Top-rated for tech/digital experience)

2025 Best Health Insurance (Looking Back)

For context, in 2025, the “best” plans were those that utilized the extended American Rescue Plan subsidies. Since those specific subsidies expired on December 31, 2025, the market for 2026 has shifted slightly. In 2025, many people found 0premiumplans;in2026,thosesameplansmightcost0premiumplans;in2026,thosesameplansmightcost10-$50/month, but are still highly subsidized.

2026 Health Insurance Comparison (The Current Year)

In 2026, the primary comparison points are:

- Network Type: PPO (More freedom, higher cost) vs. HMO (Cheaper, less freedom).

- Deductible: High Deductible (Cheap monthly) vs. Low Deductible (Expensive monthly).

- Subsidies: Crucial Update: The extra savings from the pandemic era ended Dec 31, 2025. If you qualified for savings in 2025, you will likely pay more in 2026, but you should still apply to see if you qualify for the standard Premium Tax Credit.

Part 3: The Cost Question ($0 Deductible & ACA Secrets)

This section addresses the most searched financial questions: Can I get insurance for free? Is zero deductible a trick?

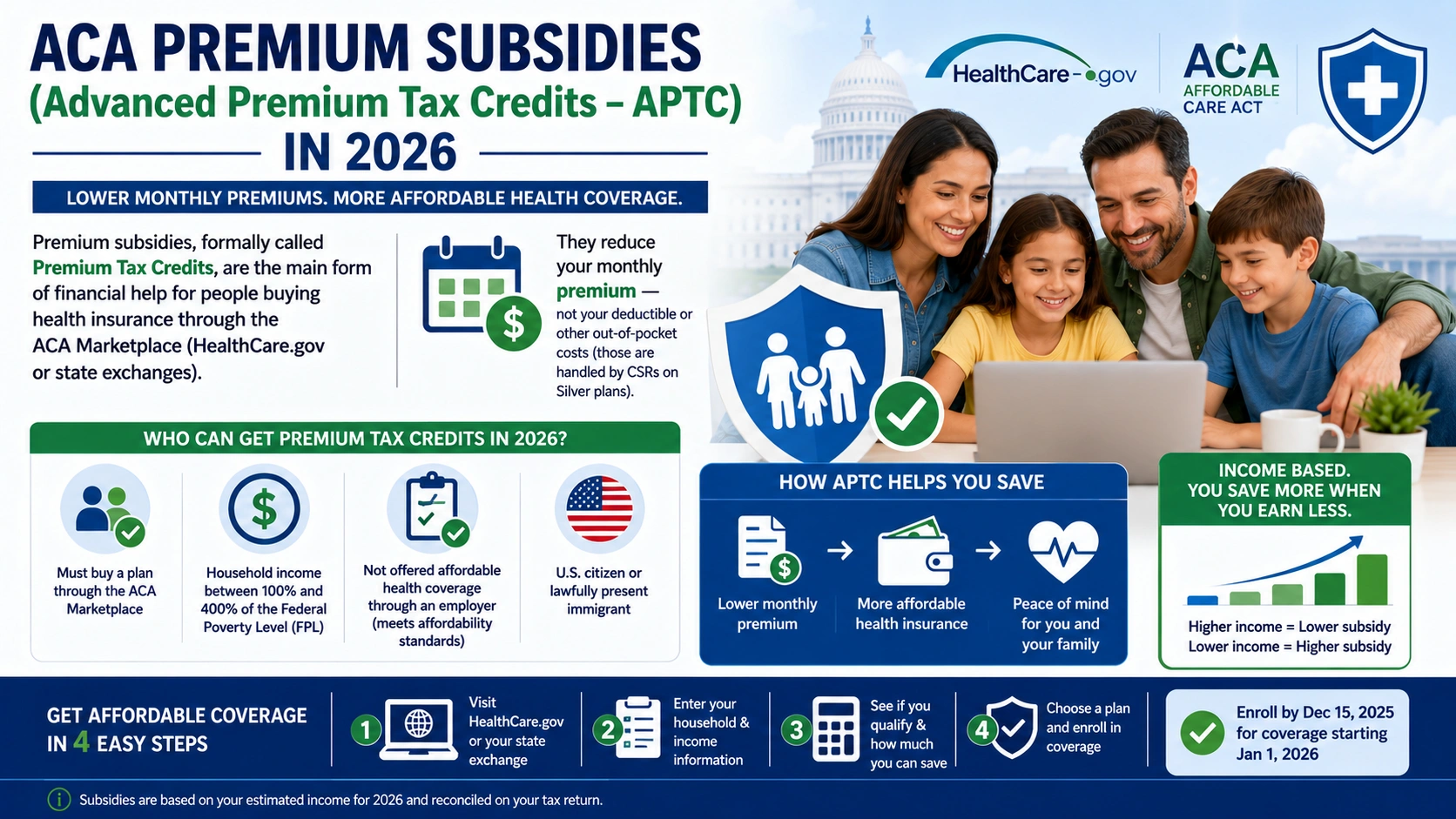

0 ACA Health Insurance & 0 a Month ACA Health Insurance

The Short Answer: Yes, you can get a $0 premium plan in 2026 if your income is low enough.

The Long Answer: “$0 a month” refers to the Premium Tax Credit (PTC) . The government pays your monthly bill directly to the insurance company.

- Eligibility: You generally qualify if your household income is between 100% and 400% of the Federal Poverty Level (FPL) .

- The 2026 Income Limits for $0 Premiums:

Warning: You must update your income if you get a raise. If you earn more than you estimated, you will have to pay back the subsidy during tax season.

$0 ACA Health Insurance Fort Lauderdale (Why location matters)

While you asked about Fort Lauderdale specifically, the principle applies to Florida and Texas alike: Rates are zip-code specific.

- In Fort Lauderdale (FL), carriers like Florida Blue and Oscar compete heavily. Because of high competition, $0 plans are very common for lower-income residents.

- Action Step: Enter your exact zip code on Healthcare.gov. A plan that is 0inFortLauderdalemightcost0inFortLauderdalemightcost20 in a rural part of the state due to fewer hospitals competing.

$0 Deductible Health Insurance

What does it mean?

A **0deductible∗∗meansyourinsurancestartspayingimmediately.Youdonothavetospend0deductible∗∗meansyourinsurancestartspayingimmediately.Youdonothavetospend1,000 or $5,000 out of pocket before coverage kicks in.

$0 Deductible Health Insurance: Good or Bad?

- Good: If you visit the doctor often, take expensive medications, or have a chronic condition, a 0deductiblesavesyouhugeamountsofmoney.Youpayaflatcopay(0deductiblesavesyouhugeamountsofmoney.Youpayaflatcopay(20-$50) for visits immediately.

- Bad: Premiums for $0 deductible plans are very high. You are essentially paying the insurance company up front to avoid a later bill.

The “Reddit” Verdict: Most personal finance experts on Reddit argue that **0deductibleis”bad”forhealthyyoungpeople∗∗.Youarelikelypayinganextra0deductibleis“bad“forhealthyyoungpeople∗∗.Youarelikelypayinganextra200/month in premiums to avoid a risk you probably won’t face. For those with chronic illness, it is “good” and often essential.

$0 Deductible Health Insurance Meaning:

Simply put: You have zero responsibility before coverage starts. It is the opposite of a “High Deductible Health Plan (HDHP).”

Part 4: Timing & Duration (Short-Term & COBRA)

What if you only need insurance for a few weeks? Or you turn 26?

1 Month Health Insurance Plan & 30 Day Health Insurance

Yes, these exist, but with strict limits. This is usually called Short Term Medical Insurance (STM) .

Key Facts for 30-Day Plans:

- Duration: You can buy a plan for exactly 30 days, 60 days, or up to 364 days depending on the state.

- Cost: Very cheap (often 50−50−150/month) because they cover catastrophes (accidents, hospitalizations) but not routine care.

- The Catch: They generally do not cover pre-existing conditions (like asthma, diabetes, or pregnancy).

- Ideal for: People between jobs who are healthy and just need a safety net for a car accident or sudden illness.

2nd Health Insurance Plan (Dual Coverage)

Can you have two plans? Yes. This is often called “Secondary Insurance.”

- Why do it? To cover costs the primary plan won’t. For example, if your primary plan has a 5,000deductible,asecondary”HospitalIndemnity”planmightpayyou5,000deductible,asecondary“HospitalIndemnity“planmightpayyou1,000 cash if you are admitted.

- Coordination of Benefits: You cannot “double dip” to make money. The two insurance companies talk to each other to ensure you never get paid more than 100% of the bill.

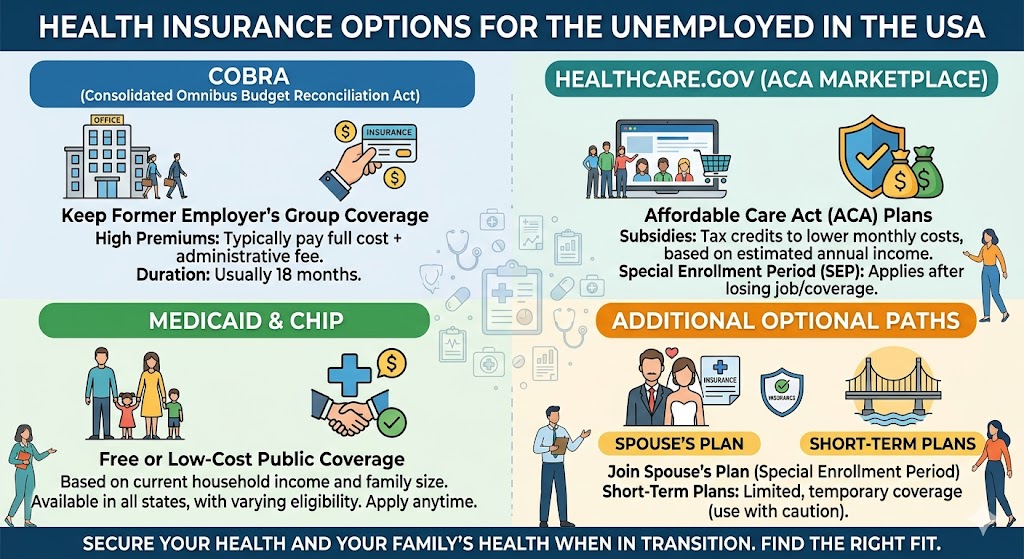

COBRA (The 18-Month Bridge)

If you leave a job, you can keep your employer plan via COBRA. However, you pay 100% of the premium (plus 2% admin fee). For a family plan in Texas, this can be $2,500+ per month. It is best used if you have already met your deductible for the year.

Part 5: Demographics (Age, Family & Parents)

Insurance rules change drastically based on your age and family status.

65 and Older Health Insurance (Medicare)

If you are 65+, you generally leave the “Marketplace” and move to Medicare.

- Medicare Part A (Hospital): Usually premium-free.

- Medicare Part B (Medical): Standard premium is about $174.70/month in 2026 (higher for high earners).

- Medicare Advantage (Part C): Private plans that replace Original Medicare.

- Medigap (Supplement): Covers the 20% that Medicare doesn’t.

Important: Do not buy an ACA Marketplace plan at 65. You will lose your subsidies and pay full price. Enroll in Medicare during your Initial Enrollment Period (3 months before your 65th birthday).

26 Parents Health Insurance (The Under-26 Rule)

Thanks to the ACA, you can stay on your parent’s health insurance plan until you turn 26 years old.

The Details:

- Marriage: It does not matter if you are married (though your spouse and kids usually cannot join).

- Location: It does not matter if you live in a different state (though the network might not cover doctors there).

- Job: It does not matter if you have a job offer (though if your job offers insurance, you might be required to take it instead).

- Turning 26: You get a Special Enrollment Period. You have 60 days before or after your 26th birthday to get your own plan (or lose coverage).

Part 6: Special Situations (Employer & Unemployed)

7 Eleven Health Insurance

Searching for “7 Eleven health insurance” likely means you are a convenience store employee or franchisee looking for benefits.

The Reality:

- If you are a Corporate Employee (7-Eleven Inc.): Large employers like this (corporate headquarters, distribution centers) are required to offer ACA-compliant health insurance to full-time employees (30+ hours/week). You would get a benefits packet with options from major carriers like UHC or BCBS.

- If you are a Franchise Store Owner: You are technically a Small Business Owner. You are not an employee of “7 Eleven” for health benefits. You must buy insurance on the ACA Marketplace or through a small business group plan.

- If you are a Minimum Wage Store Clerk: Many franchise stores do not offer insurance to part-timers. Your best bet is applying for Medicaid (if your state expanded it) or heavily subsidized Marketplace plans (which can be 0−0−50/month based on low income).

What is the Best Health Insurance for Small Business Owners in Texas?

Since this was a previous query, let’s summarize the 2026 strategy for Texas business owners:

- ICHRA (Individual Coverage HRA): The #1 pick. You set a budget ($200/month per employee), and they buy their own ACA plan. You save 30-50% vs traditional group plans.

- QSEHRA: Best for 1-50 employees. Simpler than ICHRA but has contribution limits (approx $6,450/year for singles).

- Traditional Group Plan (BCBS TX or UHC): Only necessary if you have 10+ employees who want a PPO network and you are willing to pay 50%+ of their premium.

Glossary: Your Quick-Fire Q&A

Q: Does short-term insurance cover pre-existing conditions?

A: Generally, No. Most STM plans explicitly exclude them. If you have a chronic illness, you need an ACA plan.

Q: Can I be denied coverage?

A: For ACA Plans (Marketplace): No. For Short-Term Plans: Yes, based on your medical history.

Q: What is the penalty for having no insurance in 2026?

A: There is no federal penalty (eliminated in 2019). However, a few states (CA, MA, NJ, RI, DC) have their own penalties. Texas has no penalty for being uninsured.

Q: How do I get my health insurance card fast?

A: ACA plans can take 2-3 weeks by mail. Most carriers (like Oscar, UnitedHealthcare) now offer digital ID cards instantly upon payment via their mobile app.

Q: Does Texas have expanded Medicaid?

A: No. Texas is a non-expansion state. If you are a low-income adult (18-64) without children, you likely do not qualify for Medicaid, but you do qualify for large subsidies on the Marketplace.

Final Verdict: Where Do You Start?

If you are 65+: Go to Medicare.gov. Do not pass Go.

If you are under 26 & parents have insurance: Ask to stay on their plan. It is your cheapest option.

**If you are low income (e.g., 20k/year):∗∗Goto∗∗Healthcare.gov∗∗.Youarelookingfora20k/year):∗∗Goto∗∗Healthcare.gov∗∗.Youarelookingfora0 premium Silver plan.

If you are healthy & between jobs for 2 months: Buy a Short Term Medical plan for $50/month.

If you own a business: Hire a broker to set up an ICHRA.

Health insurance in 2026 is about knowing the rules of the game. Use this guide as your playbook