Losing your job or leaving the workforce brings plenty of stress. Worrying about a medical bill shouldn’t add to it. While the question “How do I get health insurance without a job?” feels complicated, the answer is actually very structured.

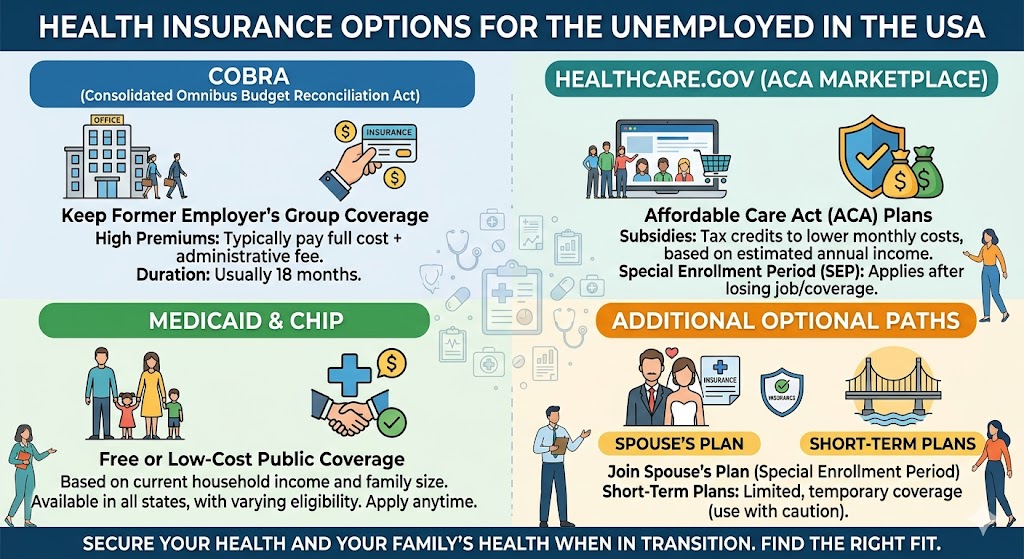

In 2026, you have four main pathways to coverage, ranging from free government programs to private plans designed for short-term gaps. Here is your roadmap to getting covered without a W-2.

1. The Health Insurance Marketplace (Your Best Bet)

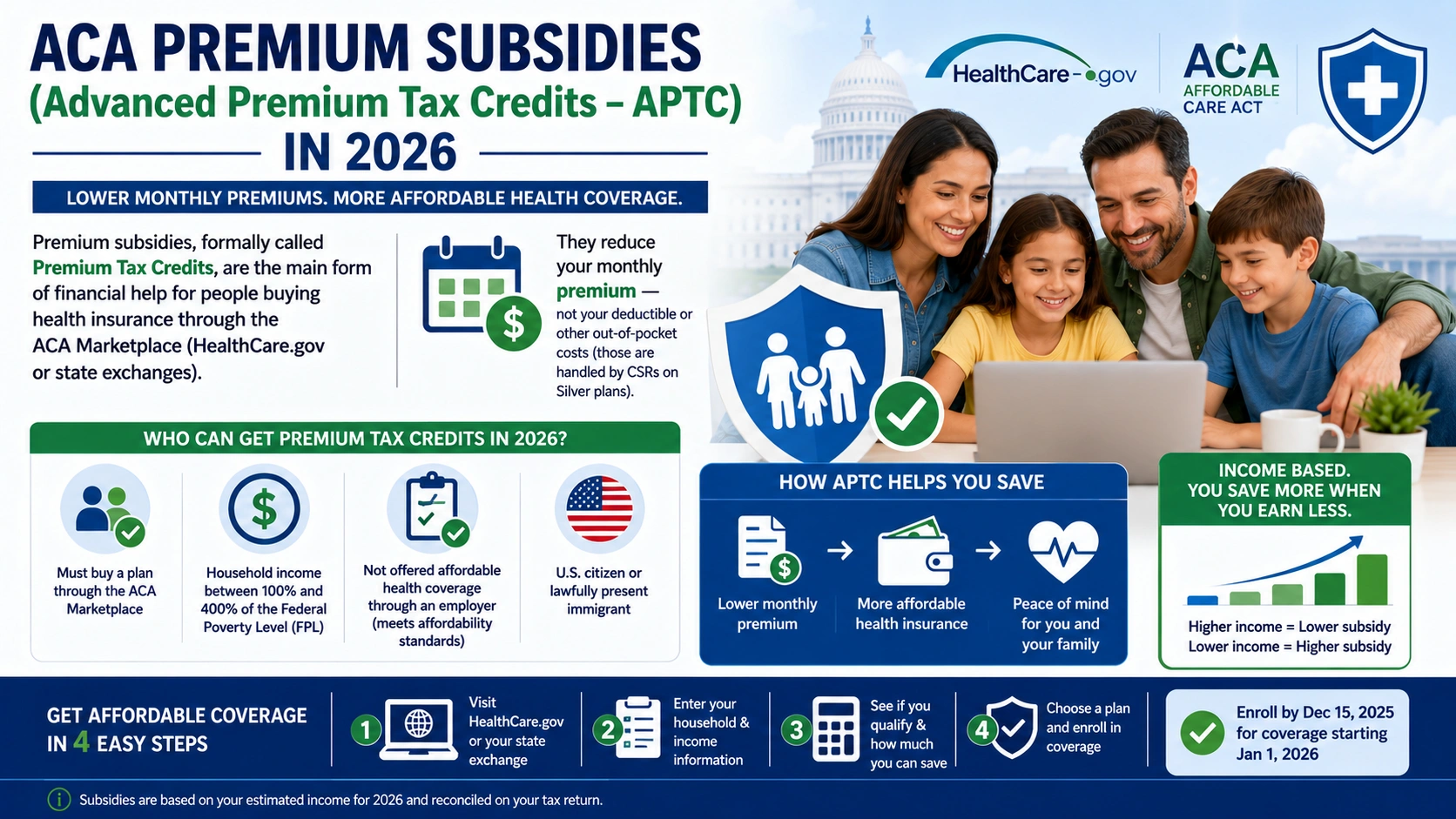

If you don’t have a job, your first stop should be HealthCare.gov. The Affordable Care Act (ACA) Marketplace was specifically designed to help people who don’t have access to employer coverage .

What you need to know for 2026:

- Open Enrollment: Runs from November 1 to January 15. If you enroll by December 15, coverage starts January 1 .

- Special Enrollment: If you just lost your job, that counts as a “qualifying life event.” You usually have 60 days before or after the job loss to enroll outside the Open Enrollment window .

Why this is the best option: ACA plans cannot deny you for pre-existing conditions. They also cover the “10 Essential Health Benefits,” including mental health, prescriptions, and maternity care . If you have low or no income right now, you may qualify for significant premium tax credits (subsidies) that drop your monthly bill drastically, potentially to $0 .

2. Medicaid & CHIP (If You Have Kids or Low Income)

Texas has a reputation for strict Medicaid rules. As of 2026, Texas has NOT expanded Medicaid to all low-income adults. However, if you have children or are pregnant, the rules change completely.

Who qualifies in Texas?

- Children: If your kids need insurance, the income limits are generous. Children in families earning up to 201% of the Federal Poverty Level (FPL) likely qualify for CHIP (Children’s Health Insurance Program) . For a family of three, that is roughly $55,000 a year .

- Pregnant Women: If you are pregnant and jobless, you likely qualify for CHIP Perinatal. This covers prenatal care, delivery, and the baby’s first year, even if your immigration status is complicated .

- Parents/Caretakers: Unfortunately, if you are a childless, non-disabled adult under 65, you generally do not qualify for traditional Medicaid in Texas regardless of how low your income is, which is why the Marketplace (with subsidies) is your backup plan .

3. COBRA (Expensive but Familiar)

When you lose your job, your employer is legally required to offer you COBRA. This allows you to keep the exact same insurance plan you had at work .

The Sticker Shock Warning:

While you were working, your employer paid a chunk of your premium. On COBRA, you pay 100% of the premium plus a 2% admin fee . For 2026, this is often very expensive.

- Sample Texas COBRA Rates for 2026: For a standard PPO plan, an individual might pay 866permonth∗∗.Forafamily,costsoftenexceed∗∗866permonth∗∗.Forafamily,costsoftenexceed∗∗2,600 per month .

- When to use it: Only use COBRA if: 1) You have already met your deductible for the year, or 2) You are in the middle of expensive medical treatment (like chemo or surgery) and don’t want to switch doctors.

4. “Group of One” Plans (For Business Owners)

Do you have a side hustle? Do you consult? Even if you have zero employees, you might qualify for a “Group PPO” plan.

In Texas, specific trusts and associations (like the TMA Insurance Trust for physicians, though other industries have analogs) allow sole proprietors to buy group coverage. Group plans usually have better networks and lower deductibles than individual plans .

How to access this: If you have a business tax ID (EIN) or file a Schedule C, contact a local independent broker who specializes in “True Group” plans for solos. You usually must enroll during November/December for a January 1 start date .

Avoid the “Cheap” Trap: A Warning on Short-Term Plans

You will see ads for very cheap plans (50−50−100/month). These are Short-Term Limited Duration Insurance (STLDI) . While legal in Texas, they are dangerous if you have no income.

- The Risk: These plans do not cover pre-existing conditions. Worse, they use “post-claims underwriting.” This means if you break your leg and file a claim, the insurance company will dig through your medical records then and cancel your policy if they find you forgot to mention a past knee injury .

- The 2026 Update: Most Texas short-term plans only last 3–4 months, though a few 12-month options exist .

- Who should buy one: Only healthy people under 65 who missed the ACA enrollment deadline and simply want a “catastrophic” shield against a car accident.

The “No Income” Problem (And How to Fix It)

Here is the biggest hurdle for unemployed people applying on Healthcare.gov: The system asks for your annual income.

If you answer “$0,” the system might think you should be on Medicaid (which Texas didn’t expand), creating a frustrating dead end.

The Solution: You are allowed to estimate your income for the year. If you are looking for a new job, estimate the salary you expect to earn by summer. If you are changing careers, project a modest income. **Do not put 0.∗∗Ifyoukeepyourestimatereasonable(e.g.,0.∗∗Ifyoukeepyourestimatereasonable(e.g.,15,000 – $20,000), you will qualify for massive tax credits that lower your premiums to almost nothing .

Summary: Your Action Plan

If you just lost your job in Texas today:

- Go to Healthcare.gov immediately. You have a 60-day Special Enrollment window.

- Estimate your income for the rest of 2026 (don’t put $0) to unlock premium tax credits.

- Compare Silver Plans on the Marketplace. These offer the best “cost-sharing” subsidies if your income is low .

- Only consider COBRA if you have major medical needs and want to keep your specific doctors.

- Never lie on a short-term plan application, or you could be stuck with a massive hospital bill.