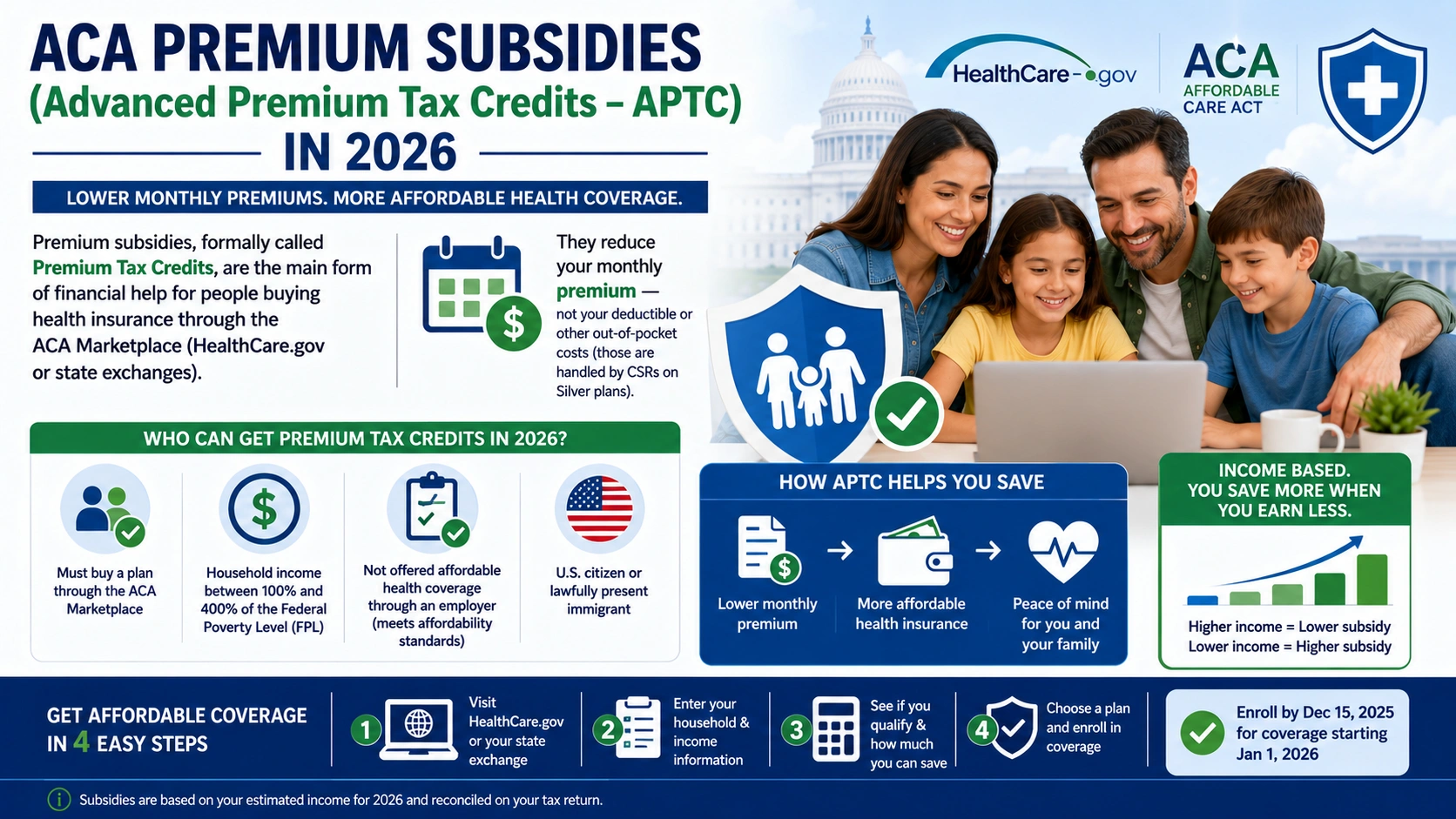

Premium subsidies, formally called Premium Tax Credits, are the main form of financial help for people buying health insurance through the ACA Marketplace (HealthCare.gov or state exchanges). They reduce your monthly premium — not your deductible or other out-of-pocket costs (those are handled by CSRs on Silver plans).

Key Changes in 2026

The temporary enhanced subsidies (from the American Rescue Plan and Inflation Reduction Act) expired at the end of 2025. For 2026 coverage:

- The subsidy cliff has returned: Eligibility ends at 400% of the Federal Poverty Level (FPL).

- Required contributions as a percentage of income are higher than in 2021–2025.

- If you receive more subsidy than you qualify for at tax time, there is no repayment cap — you may owe the full difference.

2026 Eligibility

You may qualify if:

- Household income is between 100% and 400% FPL (based on your projected income for the coverage year).

- You are not eligible for other qualifying coverage (e.g., affordable employer-sponsored insurance, Medicaid, Medicare, etc.).

- You are a U.S. citizen/national or lawfully present immigrant.

- You are not incarcerated.

2026 FPL Guidelines (48 Contiguous States)

| Household Size | 100% FPL | 400% FPL |

|---|---|---|

| 1 person | $15,650 | $62,600 |

| 2 people | $21,150 | $84,600 |

| 3 people | $26,650 | $106,600 |

| 4 people | $32,150 | $128,600 |

| Each additional | +$5,500 | +$22,000 |

Alaska and Hawaii have higher amounts. In Medicaid expansion states, people below ~138% FPL usually qualify for Medicaid instead of Marketplace subsidies.

How Premium Subsidies Are Calculated

The subsidy is based on the benchmark plan — the second-lowest-cost Silver plan in your area.

Formula: Subsidy = Benchmark Premium – Your Required Contribution

Your required contribution is a percentage of your household income, determined by IRS “applicable percentages” that increase with income.

2026 Applicable Percentages (Original ACA Rules)

| Income (% of FPL) | Max % of Income You Pay Toward Benchmark Premium |

|---|---|

| 100% – 150% | 2% – 4% |

| 150% – 200% | 4% – 6.6% |

| 200% – 250% | 6.6% – 8.5% |

| 250% – 300% | 8.5% – 9.8% |

| 300% – 400% | 9.8% |

- Lower income → larger subsidy (often $0 premium for the benchmark or cheapest plans).

- At 400% FPL → You pay the full benchmark premium (subsidy = $0).

Real-World Examples (Approximate, Single Person, Age 40)

| Annual Income | % of FPL | Approx. Required Contribution | Possible Monthly Subsidy (if benchmark is $500/mo) |

|---|---|---|---|

| $20,000 | ~128% | ~2–3% | $480+ (often $0 premium plans) |

| $30,000 | ~192% | ~5–6% | $400–$450 |

| $45,000 | ~288% | ~9% | $250–$300 |

| $60,000 | ~383% | 9.8% | $100–$150 |

| $65,000+ | >400% | 100% | $0 (full price) |

Note: Actual subsidies vary significantly by age, location, and local plan prices. Older adults and people in high-cost areas get larger absolute subsidies.

How to Get Subsidies

- Apply at Healthcare.gov (or your state Marketplace) during Open Enrollment or a Special Enrollment Period.

- Estimate your 2026 household income accurately (Modified Adjusted Gross Income – MAGI).

- The system calculates your APTC and shows you subsidized prices.

- You can choose how much APTC to take in advance (to lower monthly bills) or claim it all at tax time.

- Reconcile on your tax return (Form 8962) — income changes can mean owing money back (no cap in 2026).

Interaction with CSRs

- You can receive both premium subsidies (APTC) and Cost-Sharing Reductions if your income is 100–250% FPL.

- CSRs only apply to Silver plans and reduce deductibles/copays/OOPM.

Bottom Line: Premium subsidies remain a powerful tool in 2026 for households earning up to ~$62,600 (single) to $128,600 (family of 4), but they are less generous than in recent years. Always run your specific numbers on Healthcare.gov — local premiums and your age have a huge impact.

Would you like examples for a specific household size, age, state, or income level? Or a comparison of total costs (premium + estimated out-of-pocket) across metal levels?