Because of the joint federal-state structure you mentioned earlier, there isn’t one universal “Medicaid app.” The “how” of applying depends significantly on which state you live in and which “door” you use to enter the system.

Here is the general pathway for applying for Medicaid in the United States.

Step 1: Gathering Information

The complexity you noted regarding eligibility means you need a lot of documentation ready before you start the application.

- Proof of Identity: Driver’s license, state ID, birth certificate, or U.S. passport.

- Proof of Address: Rent receipt, utility bill, or mortgage statement.

- Income Verification: This is the most crucial part. You’ll need pay stubs, W-2 forms, or your most recent tax return (usually the 1040 form). If you are self-employed, you will need detailed records of income and expenses.

- Proof of Household Size: Social Security numbers for all members of the household.

- Immigration/Citizenship Status: If applicable, non-citizens will need their green card, USCIS number, or other valid documentation.

- Additional Documents (For Seniors/Disabled Applicants): This group (Non-MAGI) often faces an “asset test.” This requires bank statements, retirement account records, and details on property or vehicle ownership.

Step 2: The Two main “Doors” to Apply

There are generally two major avenues for applying for Medicaid: the Federal Marketplace and the State Agencies.

1. The Federal Health Insurance Marketplace (Healthcare.gov)

This is the “single streamlined application” created by the Affordable Care Act (ACA).

- When to use it: You should generally use Healthcare.gov if you are under 65, not disabled, and are a low-income adult, child, or parent.

- How it works: When you fill out the application on Healthcare.gov, you provide your information (household size, income, etc.). The system automatically calculates your Modified Adjusted Gross Income (MAGI).

- The Result: The system acts as a central triage point. It determines if you are likely eligible for Medicaid in your state. If so, Healthcare.gov automatically transfers your application information to your state’s Medicaid agency for final processing and enrollment. If you are not eligible for Medicaid, the system directs you to options for purchasing private health insurance, often with financial subsidies.

2. Your State’s Specific Medicaid Agency (or Social Services)

This is the “traditional” door.

- When to use it: You must use this route if you are applying based on being 65 or older, or if you are applying based on a disability (Non-MAGI pathway). These pathways require a more detailed evaluation that the MAGI-based Marketplace cannot perform. (Note: People under 65 can also use the state route, but Healthcare.gov is often easier for them.)

- How it works: Each state has its own application portal, paper forms, and phone hotlines. You apply directly to the state department that administers Medicaid (e.g., the Department of Health and Human Services, Department of Family Services).

Step 3: Submission and Verification

After you submit the application (via either door):

- State Review: The state Medicaid agency will receive and review your information.

- Request for Documentation: While Healthcare.gov tries to verify income electronically, the state will often follow up and mail you a formal “request for information,” asking for physical copies of the documents you gathered in Step 1 (pay stubs, etc.).

- Timeline: States are federally required to process most applications within 45 days. If the application is based on a disability (which may require a separate, longer determination process), the state has 90 days.

Step 4: The Determination and Final Steps

You will receive an official approval or denial letter in the mail.

If Denied: The denial notice must clearly state the reason for the decision (e.g., “Income too high”). Critically, the letter will also provide instructions on how to appeal the decision. You have a legal right to a fair hearing if you believe the state made an error.Medicaid Eligibility Overview (2026)

If Approved: The letter will specify the start date of your coverage (Medicaid coverage is often retroactive, sometimes covering up to three months of health expenses incurred before you applied). You will then receive your Medicaid card and often have to select a Managed Care Organization (MCO)—this is the actual health plan or insurer that will manage your care in your state.

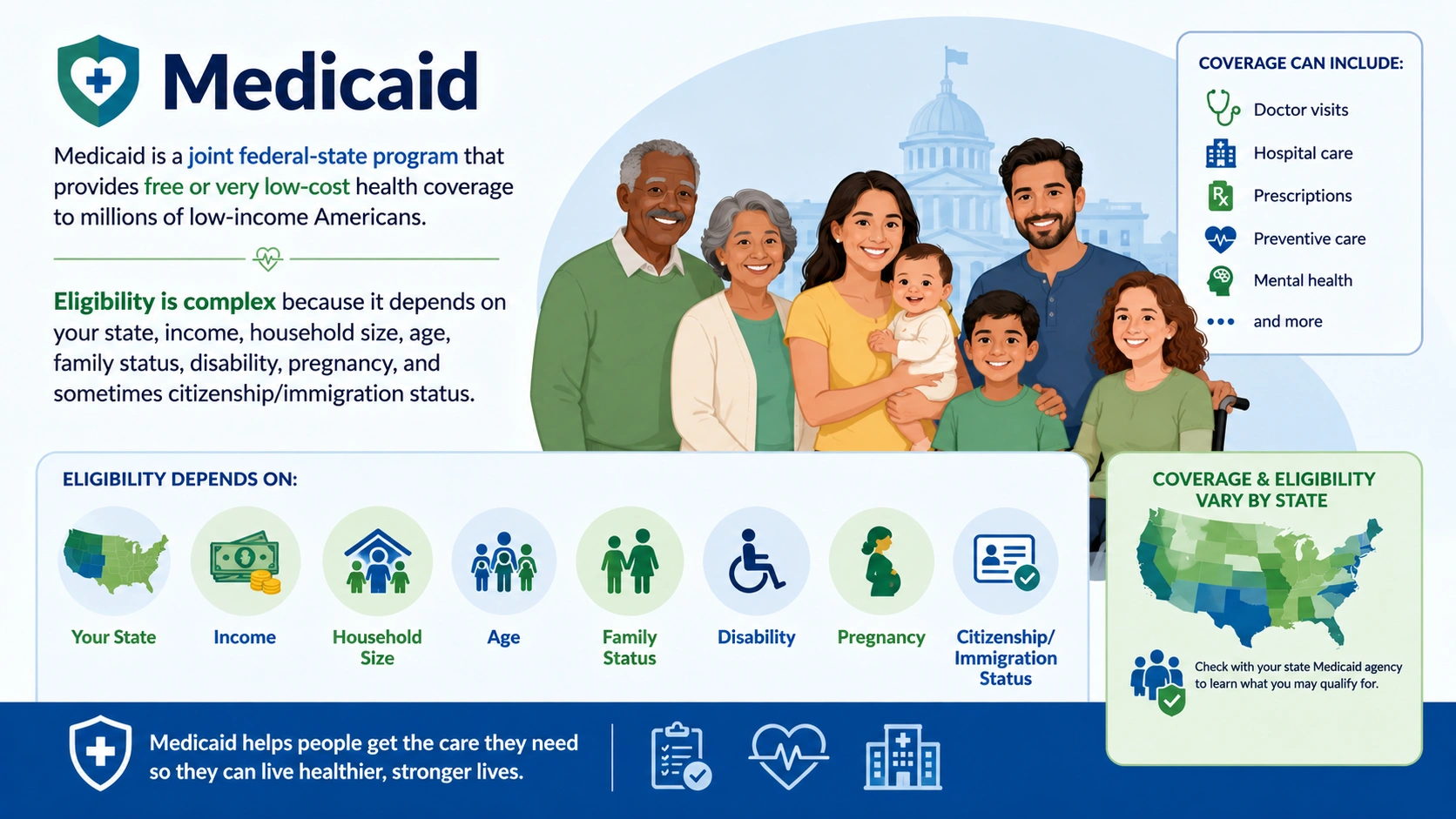

Medicaid is a joint federal-state program that provides free or very low-cost health coverage to millions of low-income Americans. Eligibility is complex because it depends on your state, income, household size, age, family status, disability, pregnancy, and sometimes citizenship/immigration status.

2026 Federal Poverty Level (FPL) – Contiguous 48 States

- 1 person: $15,960 annual (~$1,330/month)

- Family of 2: $21,640

- Family of 3: $27,320

- Family of 4: $33,000

- Add ~$5,680 per additional person.

(Alaska and Hawaii have higher limits.)

Two Main Pathways for Adults

- MAGI Medicaid (Modified Adjusted Gross Income) — Most common for children, pregnant women, parents, and expansion adults.

- Non-MAGI — For seniors (65+), people with disabilities, and long-term care (more complex income/asset rules).

Medicaid Expansion (Biggest Difference by State)

- Expansion states (41 states + DC): Low-income adults (19–64) without dependents can qualify based primarily on income up to 138% FPL (~$22,025/year or $1,835/month for a single person). Unemployment often qualifies people easily.

- Non-expansion states (as of 2026, including Texas): Childless adults generally do not qualify no matter how low their income, unless they are pregnant, disabled, or fit another category. This creates a “coverage gap” for many.

Non-expansion states typically include: Alabama, Florida, Georgia, Kansas, Mississippi, South Carolina, Tennessee, Texas, Wisconsin (partial), Wyoming, and a few others.

Key Eligibility Groups & Typical Limits (2026)

| Group | Typical Income Limit | Notes |

|---|---|---|

| Children | Up to 138–300%+ FPL (varies widely) | Often higher limits via Medicaid or CHIP |

| Pregnant Women | 138–200%+ FPL | Very common eligibility pathway |

| Parents/Caretakers | Varies (often lower than expansion) | Higher in expansion states |

| Childless Adults (19–64) | 138% FPL in expansion states | Usually ineligible in non-expansion states |

| Seniors (65+) & Disabled | Often SSI level (~$994/month) or higher optional limits | Asset tests usually apply ($2,000 individual) |

| Long-Term Care / Nursing Home | Varies; often ~$2,982/month income cap | Strict asset limits (~$2,000) |

Texas-Specific Medicaid Eligibility (Non-Expansion State)

Texas has not expanded Medicaid. This means:

- Childless adults under 65 generally cannot qualify based on income alone.

- Parents may qualify at lower income levels (often tied to very low thresholds for families).

- Disabled, blind, elderly, or pregnant individuals have separate pathways, often linked to SSI (Supplemental Security Income) eligibility (~$994/month for an individual in 2026).

- Children have better access through Medicaid (STAR) or CHIP.

Texas Income Examples (approximate for 2026):

- Children’s Medicaid: Often lower thresholds (e.g., family of 4 around $3,564/month or less).

- CHIP: Higher tier (see previous responses).

Important 2026 Developments

- Work requirements: New or expanded rules for certain adults (ages 19–64) in expansion populations, requiring 80+ hours/month of work, school, or community engagement in many cases. Implementation begins in 2026–2027.

- More frequent redeterminations: States must review eligibility more often.

- Immigration changes: Restrictions on eligibility for some lawfully present immigrants.

- Unemployment impact: Counts as income but often lowers total household income enough to qualify in expansion states.

How to Check & Apply

- Best starting point: Visit Healthcare.gov — one application screens for Medicaid, CHIP, and ACA subsidies.

- State-specific: Search “[Your State] Medicaid eligibility” or visit your state’s HHSC/Medicaid website (e.g., YourTexasBenefits.com for Texas).

- Gather: Income proof, residency, citizenship/immigration docs, household info.

- Apply anytime (no open enrollment).

Recommendation: Even if you think you might not qualify, apply anyway — the system determines eligibility automatically, and rules vary by household details. Eligibility can change with income fluctuations (e.g., job loss).

Would you like details for a specific state, household size, category (e.g., parents, disabled, seniors), or a comparison with ACA subsidies/CHIP? Let me know your situation for more tailored examples!Medicaid vs. ACA Marketplace Subsidies (Premium Tax Credits + CSRs)

Both programs help lower-income and unemployed Americans afford health coverage, but they differ significantly in eligibility, costs, benefits, and experience. Here’s a clear side-by-side comparison for 2026.

1. Overview

- Medicaid: Government-funded program providing free or very low-cost comprehensive coverage. Primarily for very low-income individuals.

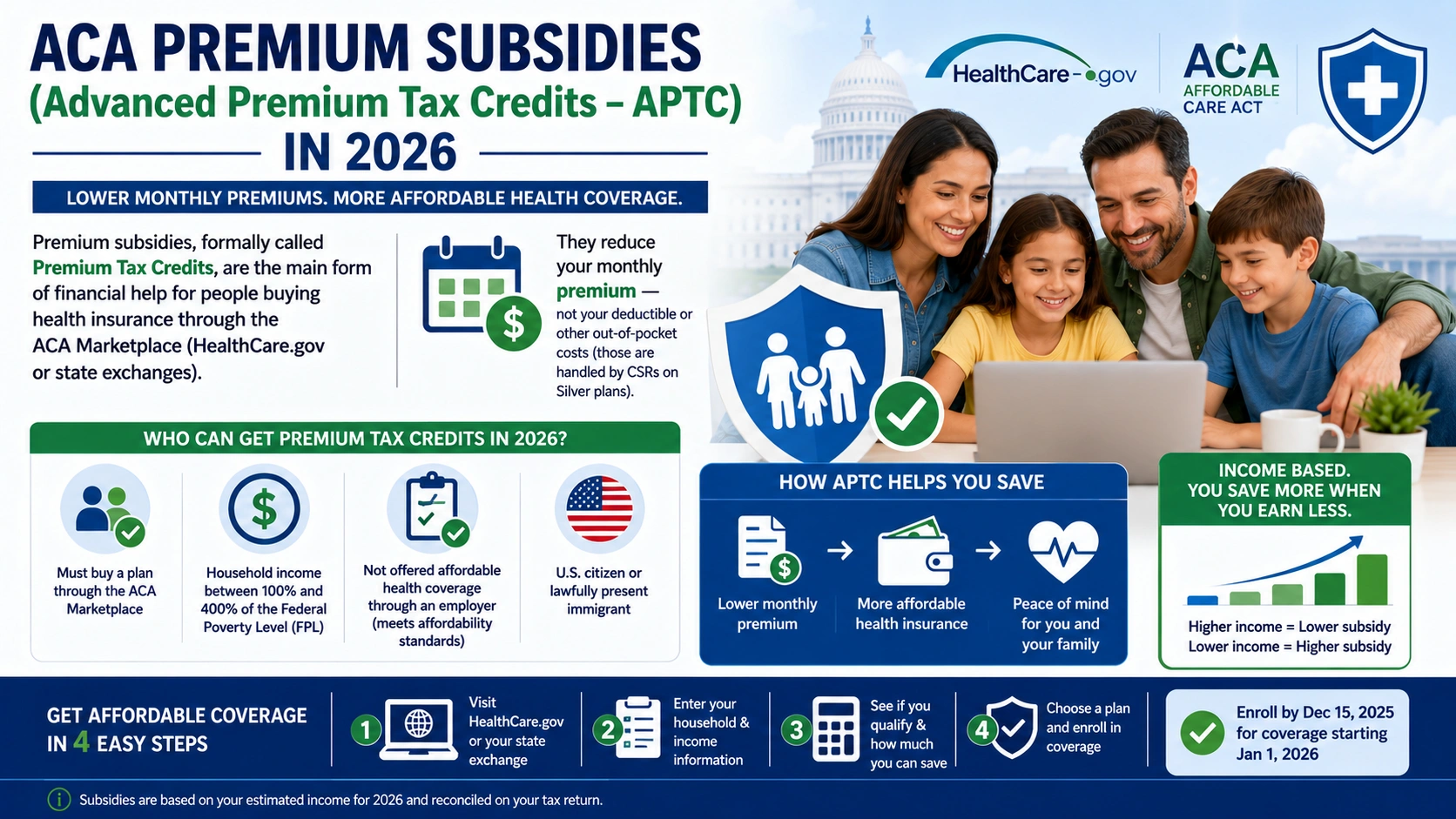

- ACA Subsidies (APTC + CSRs): Financial assistance to buy private insurance on the Marketplace (HealthCare.gov or state exchange). Premium subsidies lower monthly payments; Cost-Sharing Reductions (CSRs) lower deductibles/copays (only on Silver plans).

2. Eligibility Comparison

| Factor | Medicaid | ACA Marketplace Subsidies |

|---|---|---|

| Income Range | Usually up to 138% FPL in expansion states | 100%–400% FPL (subsidy cliff at 400%) |

| State Variation | Huge differences (expansion vs non-expansion) | Federal rules, but premiums vary by location |

| Expansion States (41 states + DC) | Adults up to ~138% FPL (~$22,025 single / ~$45,540 family of 4) | Starts above 138% FPL |

| Non-Expansion States (e.g., Texas, Florida) | Very limited for childless adults | Starts at 100% FPL (creates “coverage gap”) |

| Other Factors | Household size, pregnancy, disability, children, citizenship | Ineligible for “affordable” employer coverage or Medicaid |

| Unemployed Impact | Often qualifies due to low income | Special Enrollment Period triggered by job loss |

2026 FPL Examples (Contiguous U.S.):

- 1 person: 138% ≈ $22,025 | 400% ≈ $63,840

- Family of 4: 138% ≈ $45,540 | 400% ≈ $128,600

3. Costs to You

| Aspect | Medicaid | ACA Subsidies |

|---|---|---|

| Premiums | Usually $0 | Reduced by subsidies (can be $0–low for many) |

| Deductibles/Copays | Usually $0 or very low | Reduced via CSRs (if income ≤250% FPL on Silver) |

| Out-of-Pocket Max | Very low or none | Up to ~$10,600 individual (lower with CSRs) |

| Best for | Very low income | Moderate income (especially 150–400% FPL) |

CSRs (extra help with out-of-pocket costs) are available only on Silver plans for incomes 100–250% FPL.

4. Coverage and Benefits

| Feature | Medicaid | ACA Marketplace Plans |

|---|---|---|

| Benefits | Comprehensive (including long-term care, nursing homes, transportation in many cases) | 10 Essential Health Benefits + preventive care |

| Provider Network | Often limited (varies by state) | Varies by plan (HMO/PPO/EPO) |

| Prescription Drugs | Usually excellent coverage | Varies by plan formulary |

| Pre-existing Conditions | Covered | Covered |

| Dental/Vision (Adults) | Often covered (varies) | Usually not (except children) |

5. Pros & Cons

Medicaid Pros:

- Lowest or no cost

- Comprehensive benefits

- No network worries in some states

- Automatic screening via one application

Medicaid Cons:

- Strict eligibility (especially non-expansion states)

- Possible work requirements in some states

- Provider access can be limited

- Asset tests in some categories

ACA Subsidies Pros:

- Broader income eligibility

- More plan choices and provider networks

- Can keep the same doctors more easily

- Works with higher incomes

ACA Subsidies Cons:

- Still have deductibles/copays (even with CSRs)

- Premiums can rise sharply above 400% FPL

- Must pay premiums monthly

- Less generous in 2026 after enhanced subsidies expired

6. Application & Enrollment

- Both: Start at Healthcare.gov — one application automatically screens for Medicaid, CHIP, and subsidized Marketplace plans.

- Medicaid: Apply anytime; ongoing eligibility reviews.

- Marketplace: Annual Open Enrollment + Special Enrollment (e.g., after job loss).

Recommendation for Unemployed People

- Very low income (under ~138% FPL): Apply for Medicaid first — best option if eligible.

- Moderate income (above Medicaid limit): ACA subsidies often make coverage affordable.

- In Texas (non-expansion): Many fall into the coverage gap or rely more on ACA subsidies/CHIP for kids.

Best Next Step: Go to Healthcare.gov, enter your state, household size, and estimated 2026 income. The tool will show exactly what you qualify for in minutes.

Would you like a comparison for a specific income/household size, your state (e.g., Texas), or examples of total estimated costs? Let me know!Medicare Eligibility Overview (2026)

Medicare is the federal health insurance program primarily for people age 65 and older, but it also covers certain younger individuals with disabilities or specific conditions. It is not primarily for unemployed people under 65 (unlike Medicaid or ACA Marketplace options).

Main Eligibility Categories

You qualify for Medicare if you meet any of these:

- Age 65 or Older

- Most common pathway.

- You (or your spouse) must be a U.S. citizen or lawful permanent resident for at least 5 years.

- Automatic enrollment if you’re already receiving Social Security or Railroad Retirement Board (RRB) benefits.

- Under Age 65 with a Qualifying Disability

- Receiving Social Security Disability Insurance (SSDI) for 24 months.

- Automatic enrollment usually occurs in the 25th month of SSDI benefits.

- End-Stage Renal Disease (ESRD) — Permanent kidney failure requiring dialysis or transplant.

- Eligible at any age, no 24-month waiting period.

- Amyotrophic Lateral Sclerosis (ALS / Lou Gehrig’s Disease)

- Eligible at any age, immediate upon starting SSDI benefits.

Citizenship/Residency: U.S. citizen or lawfully admitted permanent resident with 5 continuous years of residence.

Medicare Parts Overview

- Part A (Hospital Insurance): Inpatient hospital stays, skilled nursing, hospice, some home health. Most people get premium-free Part A if they (or spouse) paid Medicare taxes for at least 10 years (40 quarters).

- Part B (Medical Insurance): Doctor visits, outpatient care, preventive services, durable medical equipment. Everyone pays a monthly premium.

- Part C (Medicare Advantage): Private plans that bundle A + B (often + D).

- Part D: Prescription drug coverage.

2026 Costs (Key Figures)

- Part A Premium: $0 for most (premium-free).

- Buy-in: $311/month (30–39 quarters) or $565/month (fewer than 30 quarters).

- Part B Standard Premium: $202.90/month (up from $185 in 2025).

- Higher earners pay IRMAA surcharges (Income-Related Monthly Adjustment Amount) starting at modified adjusted gross income of $109,000 (individual) / $218,000 (joint).

- Part A Deductible: $1,736 per benefit period.

- Part B Deductible: $283 per year.

Medicare for Unemployed People

- Under 65: Unemployment alone does not qualify you. You typically need SSDI (which has its own strict disability criteria) or one of the exceptions above.

- Age 65+: You can qualify regardless of employment status, as long as you meet the age and residency rules. Many retirees or newly unemployed 65+ rely on Medicare.

- Transition from Other Coverage: Losing job-based insurance (e.g., COBRA ends) can trigger a Special Enrollment Period for Medicare if you’re already eligible.

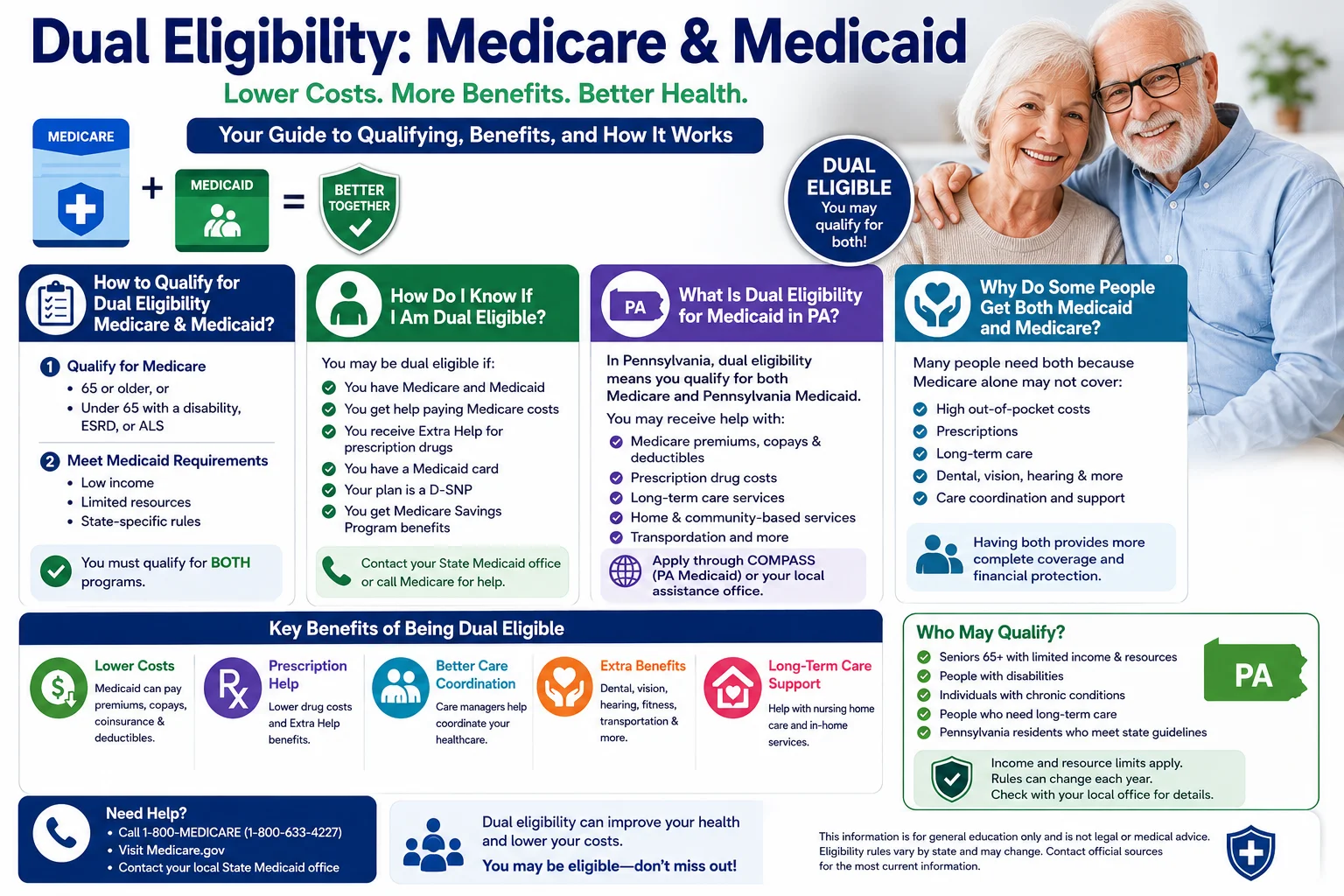

Dual Eligibility (Medicare + Medicaid)

Low-income Medicare beneficiaries may also qualify for Medicaid (called “dual eligibles”). Medicaid can help pay Medicare premiums, deductibles, and copays. This is common for people with limited income and resources.

How to Apply / Enroll

- Automatic: If receiving Social Security/RRB benefits.

- Manual: Contact Social Security Administration (ssa.gov or 1-800-772-1213) or visit Medicare.gov.

- Initial Enrollment Period (IEP): 3 months before your 65th birthday month, through 3 months after.

- Penalties: Late enrollment in Part B or Part D can result in lifelong premium penalties.

Key Differences from Other Programs (Quick Recap)

| Program | Main Eligibility | Cost to You | Best For |

|---|---|---|---|

| Medicare | 65+ or disability/ESRD/ALS | Premiums + deductibles | Seniors & long-term disabled |

| Medicaid | Low income (state-specific) | Usually $0 | Very low-income (any age) |

| ACA Subsidies | 100–400% FPL | Subsidized premiums | Working-age adults & moderate income |

For unemployed people under 65: Focus first on Medicaid, CHIP (for kids), or ACA Marketplace with subsidies. Medicare is generally not an option unless you meet the disability criteria.

Recommendation: Visit Medicare.gov or call Social Security for a personalized eligibility check. If you’re nearing 65 or have a qualifying condition, sign up promptly to avoid gaps or penalties.

Would you like details on Medicare Advantage vs Original Medicare, costs for a specific situation, dual eligibility, or how Medicare interacts with COBRA/unemployment? Let me know your age range or state for more tailored info!Medicare Advantage Plans (Part C) in 2026: A Complete Exploration

Medicare Advantage (MA) plans, also known as Part C, are private insurance plans approved by Medicare that provide an alternative to Original Medicare (Parts A + B). They bundle hospital (Part A), medical (Part B), and usually prescription drug coverage (Part D) into one plan, often with extra benefits.

Key Facts for 2026

- Enrollment: Over 35 million beneficiaries (about 51–54% of eligible Medicare population). Growth has slowed but remains strong.

- Availability: Nearly all Medicare beneficiaries (99%) have access to at least one plan; most have many choices (average ~30–40 plans per area).

- Average Premium: ~$14 per month (in addition to the standard Part B premium of $202.90). Two-thirds of plans with drug coverage have $0 additional premium.

- Out-of-Pocket Maximum (OOPM): Capped at around $8,850–$9,250 for in-network services (plans can set lower limits). Once reached, the plan covers 100% of covered services for the year.

How Medicare Advantage Works

- You must have both Part A and Part B to join.

- Plans are offered by private insurers (e.g., UnitedHealthcare, Humana, Aetna/HealthSpring, Blue Cross, etc.).

- They must cover at least what Original Medicare covers but can (and usually do) add more.

- Most include Part D prescription coverage.

Common Types of Medicare Advantage Plans

| Plan Type | Network & Flexibility | Referrals Needed? | Best For |

|---|---|---|---|

| HMO (Most common) | Strict network; limited out-of-network | Usually yes | Lower premiums, local care |

| PPO | In-network + out-of-network (higher cost) | Usually no | More flexibility |

| HMO-POS | HMO with some out-of-network options | Varies | Hybrid needs |

| PFFS | No formal network (must accept plan terms) | No | Areas with few providers |

| Special Needs Plans (SNPs) | Targeted to specific groups (dual eligibles, chronic conditions, institutional care) | Varies | People with special needs |

Major Benefits (Often Included)

- Extra perks not in Original Medicare: Routine dental, vision, hearing aids, fitness/gym memberships (e.g., SilverSneakers), transportation to appointments, over-the-counter allowances, meal delivery, and more.

- Out-of-pocket protection — unlike Original Medicare, which has no annual cap.

- Care coordination — especially in HMOs.

Pros and Cons

Pros:

- Potentially lower monthly costs and predictable maximum spending.

- Bundled coverage (one plan instead of multiple).

- Valuable extras (dental, vision, hearing).

- Many $0-premium options.

Cons:

- Provider networks — restricted in most plans (especially HMOs). You may need to change doctors.

- Prior authorization — more common for services, drugs, or procedures.

- Geographic limits — plans are local; coverage may not travel well (except emergencies).

- Annual changes — plans can alter benefits, premiums, or networks each year.

- In 2026: Some reduction in $0-premium plans, slimmer supplemental benefits, and more people forced to switch plans due to insurer exits.

Medicare Advantage vs. Original Medicare (Quick Comparison)

- Original Medicare: Unlimited provider choice nationwide, no referrals for specialists, but higher potential out-of-pocket costs (no cap unless you add Medigap + Part D). No routine dental/vision/hearing.

- Medicare Advantage: Network restrictions and possible referrals, but capped costs and extra benefits.

Dual Eligible individuals (Medicare + Medicaid) often do well in Special Needs Plans (D-SNPs).

Important 2026 Considerations

- Slight decline in overall plan availability and some $0-premium options.

- Continued focus on value-added benefits, though some trimming occurred.

- Strong growth in Special Needs Plans (SNPs).

How to Choose and Enroll

- Review your needs — Current doctors, medications, expected health usage, travel, and budget.

- Use Medicare.gov Plan Finder (or call 1-800-MEDICARE) — Compare plans by total estimated costs, not just premiums.

- Check networks — Verify your doctors and hospitals are in-network.

- Annual Enrollment Period: October 15 – December 7 for coverage starting January 1. Special Enrollment Periods apply in certain situations.

- You can switch back to Original Medicare (with or without Medigap) during open enrollment if needed.

Recommendation: Medicare Advantage works best for people who prefer lower premiums, value extra benefits, and are comfortable staying within a network. Those who travel frequently, have complex conditions requiring many specialists, or want maximum provider choice often prefer Original Medicare + Medigap + Part D.